If collective purchasing power of all poor people for goods and services is combined, it amounts to approximately $7 trillion, which is almost twice the size of Germany’s economy (China $11 trillion, USA $18 trillion). Therefore, if we consider these poor and unbanked people as an economy as a whole this is a huge financial opportunity for leverage for these poor people as well as for global communities, says Sanjali Yadav, President, End Poverty Club, Winston Churchill High School, Potomac, US, in this insightful article.

If collective purchasing power of all poor people for goods and services is combined, it amounts to approximately $7 trillion, which is almost twice the size of Germany’s economy (China $11 trillion, USA $18 trillion). Therefore, if we consider these poor and unbanked people as an economy as a whole this is a huge financial opportunity for leverage for these poor people as well as for global communities, says Sanjali Yadav, President, End Poverty Club, Winston Churchill High School, Potomac, US, in this insightful article.

Universal financial access 2020 and sustainable development goals attempt to bring people within the financial system to overcome their exclusion and integrate them in the mainstream of development. The financially excluded sections of society around the world continue to be deprived from financial leverage both individually as well as collectively.

The wealth of the people and the wealth of the nations have been created based on training and investment with a multiplier effect. However, the financially excluded people are deprived from the local system as well as the global system, and in the process, they continue to be in the trap of poverty. To break the vicious cycle of poverty, there is a need for an innovative financial approach to pull them out of this poverty trap.

The financially excluded people around the world have low spending power individually for their consumption cycle which they use to purchase goods and services for their livelihood. But, the collective buying power is tremendous. They are dependent on direct cash purchases due to which they cannot leverage on their little financial capacity for savings, investments or even for purchases on credit. Data from PovcalNet from World Bank shows that with $5.5 PP, there are 3.5 billion, who are poor and need financial leverage to come out of trap of poverty and its ill effects.

If we combine their collective purchasing power for goods and services, it amounts to approximately $7 trillion, which is almost twice the size of Germany’s economy (China $11 trillion, USA $18 trillion). Therefore, if we consider these poor and unbanked people as an economy as a whole this is a huge financial opportunity for leverage for these poor people as well as for global communities.

This will also open new possibilities and opportunities for private sector to leverage supply chain and generate efficiency in the system. Besides it will open up new opportunities to develop a new model to attack poverty and also redesign the existing global governance architecture.

The question is how this $7 trillion of poor man’s collective expenditure capacity (P-CEC) can be used to ensure that the returns from these livelihood expenditure can take care of their livelihood, and their expenditure capital can be used to earn returns and excess returns can be used to provide them social benefits. This also offers opportunities to integrate national governments’ social benefit programmes and through generation of efficiency more impact on poverty reduction.

The expenditure pattern of poor people in the following diagram indicates that poor people are financially stressed on daily basis. A study shows that poor people spend 182 percent of the income; middle class 89 percent; and rich only 61 percent. For housing, poor people spend 72 percent of income, middle class 30 percent and rich 19 percent. For transportation, the expenditure is 28 percent, 17 percent, 10 percent and for food 28 percent, 12 percent and 7 percent, respectively.

This shows that poor people with even low earning are spending more as percentage of their income on basic things in life and this continues to push them in the poverty trap. The question is how to pull them out of this trap and make their livings financially sustainable. This is the question I am trying to answer here. By increasing the financial bargaining capacity through collective approach and improved supply chain logistics on a technology platform, we can change the map of world poverty.

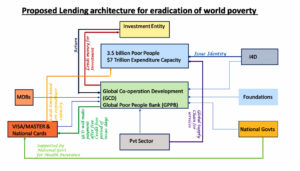

For this a GLOBAL FINANCIAL ASSISTANCE system for Poor (to be called as G-FSAP) has been proposed. The proposed structure of the system would:

For this a GLOBAL FINANCIAL ASSISTANCE system for Poor (to be called as G-FSAP) has been proposed. The proposed structure of the system would:

The diagram above is a new architecture to address the issue of global poverty, which is based on global cooperation and collaboration of MDBs, private sector, foundations and national governments. This single global entity approach will be a unique way to consolidate global resources to create an ecosystem for the welfare of poor people and this will also be the single largest welfare system on the planet. All multilateral institutions have been talking about safety nets but so far, this global safety system is missing.

Creating a system to connect poor’s globally on a single platform

Poor people continue to be marginalised and discriminated at on the basis of identity and then lack of access to credit from the financial system. Many developing countries have developed their unique identity system like Aadhar in India, which is a unique number given to citizen and services are linked with this unique number.

But many countries still continue to struggle to provide identity and access to financial system. As per a World Bank report, an estimated 1.1 billion people in the world are unable to prove their identity. That is one in every seven individuals. The majority live in Africa and Asia, and more than a third are under the age of 18.

Identity for development is an important initiative to identify global citizen. This unique initiative will enable all the people in the world to have common identifier on a single platform. This product can be used to leverage the collective expenditure capacity for financial leverage.

So far in the world the thinking has been to leverage income, but here it is proposed to leverage collective expenditure capacity of people around the world. In the proposed system, this identity will be important enabling factor. This unique identity will be used for estimating the expenditure capacity and also for issuing expenditure capacity based cards with health insurance and other social safety benefits of the Govt.

Creating a Global Entity: Global Corporation for Development (GCD)

A Global Corporation for Development maybe set up with membership to all countries as well as to private sectors like Google, Microsoft, IBM, other international organisations as well as philanthropic organisations like the Gate foundation. Private players like Visa and MasterCard and entities with expertise in global supply chain and important stakeholder to ensure the supply of goods and services at the lowest price with reliability and quality. This global alliance for development will be first-of-its-kind on the basis of public and private sector partnership for attacking poverty collectively for a collective cause and global benefits as well as for creating opportunities for all.

A pool of investment corporations and development entities like IFC and IBRD and other private players can be members of this. GCD will invest money and generate return and will pay back to card companies after interest free period. The excess returns with GCD will be used as retained earnings for further investment and will be used to lend additionally for housing loan to poor people.

Steps that can be taken

- Identity to all under I4D

- All expenditure capacity to be deposited and link with GCD

iii. Cards issued by GCD with Visa and Master Card and other local players with health benefits and purchase limit for credit free 100 days with negotiations with VISA and Master Card. This card may also contain national social benefits. This will also cut down individual countries expenditure for issuing social cards as well as other identity cards.

- Payment to cards companies will be made through GCD after credit free period.

- Private companies like Walmart, Costco, amazon, google and other local companies to be part of supply chain will supply services and goods at the most competitive prices and local goods with extended credits. They will get readymade huge global markets and will be happy to cut down prices. Also, in the process global logistics and supply set will be developed to match this huge demand.

- GCD will use money available during the credit period to invest and generate returns. It will pay credit card companies after 60-90 days . Excess returns will be used further for returns as well as for lending for housing to poor or to create global cooperatives for poor.

vii. International financial institutions like IFC may be engaged for leveraging the financial power. The private sector firms specializing in markets based returns may also be engaged to use this expenditure wealth for generating returns.

viii. MNEs in the field of insurance, health and mortgage will be invited to join this global alliance and offer products and services at much less prices as their cost of marketing will be zero and this cost will be factored into insurance prices.

- National governments have their own social programmes and have huge budgets. As a partner of this alliance, they may be encouraged to join to benefit from power of leverage for their poor people. This will bring huge political dividend to the Governments.

This alliance of NGOs, private sector, governments, insurance companies, development institutions will work for making these over three billion people realise their dream of mainstreaming into the global system with dignity of life and availability of resources.

This innovative means of mainstreaming will add to the muscle of the financial system and bring liquidity in the overall global market. This linking with ID for development where global IDs issued to the poor people to link all the benefits, services and programmes to them which can flow directly to them bypassing the bureaucracy and government system will also make world safer and will help in countering terrorism and anti-social elements.

The global savings resulting from this system could be further used through GCD to create a cycle of financial growth for poor as well as an additional input to push global growth and make world more stable.

The World in 2018 looks entirely different from how it was in 1940s when international organisations and UN were set up. The demand in today’s world has changed dramatically as world has never been connected so well before in history and it has never given impression of single world entity ever before. Around 50 percent of 7.6 billion the world population has an internet connection today. In 1995, it was less than 1 percent. The number of internet users has increased tenfold from 1999 to 2013.

The first billion was reached in 2005; the second billion in 2010; the third billion in 2014. This is unprecedented connectivity of human beings and if we take into account the connectivity of machines globally, which is around 23 billion globally and projected to rise 75 billion by 2025, then it already gives a picture of wired World.

Similarly, universal financial access to all global citizens will create a global commons of connected world digitally and financially. Never in the history was an opportunity to achieve scale of any global programme through scale, speed and technology.

This is an unprecedented opportunity to attack on poverty as common enemy of humanity and make these 3.5 billion people free from poverty. The MNEs are seen as profit machine but this perception has to be changed by capitalizing on their global network and cash reserves to make them partner in progress on this war against the poverty. The financial leverage power of the private sector can be used by the government as a partner to private sector.

This could have been unthinkable few years back but digital strategies have completely changed how traditional models of business and governance have been disrupted. Only because of disruption of traditional models, there is hope that the proposed governance model will change the world and will be a win-win opportunities to MNEs sector, governments, people and national governments.

(Views expressed in this article are of author only)